The 3 Numbers That Tell You If Your Sleep Consulting Business Is Financially Healthy

The three numbers that tell you whether your sleep consulting business is financially healthy are your total revenue, your total expenses, and your net profit margin. If you don't know these three figures right now, you're running your business on instinct rather than information. This guide walks through how to calculate them, what healthy looks like in a service business like ours, and what to do about bookkeeping, tax, business structures, and compliance, wherever in the world you're based.

This article is for general educational purposes only. It is not financial, legal, or tax advice. Rules vary significantly by country, state, and individual circumstance. Always consult a qualified accountant or tax professional in your specific jurisdiction before making financial decisions for your business.

In this guide

- The 3 numbers every sleep consultant needs to know

- Number 1: Revenue

- Number 2: Expenses

- Number 3: Net profit margin

- What healthy profit margins look like for sleep consultants

- The profit and loss statement

- Bookkeeping basics: tracking income and expenses

- Tax: how much to set aside and when to pay

- Ongoing compliance: licences, permits, and annual filings

- Frequently asked questions

What I've noticed is that most sleep consultants are confident when they're on a consultation call, writing a sleep plan, or supporting a family through a hard night. The moment the conversation turns to money (revenue, margins, tax) something shifts. Eyes glaze. Anxiety rises. The tab gets quietly closed.

Here's the problem with that. You can be an exceptional sleep consultant and a struggling business owner at the same time. Knowing your numbers doesn't make you less of a practitioner. It makes you the kind of practitioner who can actually keep doing this work for the long term, because the business is stable enough to support it.

You don't need to become an accountant. You need to understand three numbers, build one simple tracking habit, and know enough about the tax and structure rules in your country to stay compliant. That's it. Everything else builds on those foundations.

The 3 Numbers Every Sleep Consultant Needs to Know

If you only ever track three things in your business, make it these. They tell you whether you're actually making money, whether you're spending too much, and whether your business is sustainable enough to keep running.

| # | Number | What it means | What healthy looks like |

|---|---|---|---|

| 1 | Total Revenue | All money coming in before any deductions | Covers expenses + tax + profit with room to breathe |

| 2 | Total Expenses | All money going out to run the business | Below 30–40% of revenue in a lean service business |

| 3 | Net Profit Margin | What percentage of revenue you actually keep | 60–75%+ for a solo sleep consulting business |

Number 1: Revenue

Revenue is every dollar, pound, euro, or rupiah that comes into your business before you take anything out. Client packages, digital product sales, workshop tickets, affiliate income: all of it counts as revenue.

How to calculate it: Add up every payment received in a given period (monthly and annually are both useful). Use your business bank account as the source of truth. This is another reason why keeping business and personal finances completely separate is non-negotiable.

What revenue tells you: On its own, revenue doesn't tell you much. A sleep consultant bringing in $5,000 a month with $4,500 in expenses is in worse shape than one bringing in $2,500 with $400 in expenses. Revenue only becomes meaningful when you compare it to what it cost you to earn it.

Number 2: Expenses

Expenses are every cost you incur running the business. For a solo sleep consulting business, these are typically low. That is one of the great advantages of this field. Common expenses include:

- Software subscriptions (Zoom, scheduling tools, email marketing, your business platform)

- Professional development (certifications, books, courses, conferences)

- Marketing costs (website hosting, ads, photography, branding)

- Insurance premiums

- Accounting and legal fees

- Client gifts or printed materials

- Annual business registration or licence fees

How to calculate it: Add up every business-related payment made in the same period. Track every expense as it happens, not quarterly, not at tax time. One missed expense is money you paid tax on unnecessarily.

The rule on deductibility: In most jurisdictions, legitimate business expenses reduce your taxable income. A subscription to a tool you use for client work is deductible. A coffee you had while working at a café may or may not be, depending on your country's rules. When in doubt, keep the receipt and ask your accountant.

Number 3: Net Profit Margin

Net profit margin is the percentage of your revenue that you actually keep after all expenses. It's the clearest single indicator of whether your business is financially healthy.

How to calculate it:

Net Profit Margin = (Net Profit ÷ Revenue) × 100

Example: Revenue $3,000 / Expenses $750 / Net Profit $2,250 / Margin = 75%

Note: this is before tax. Your actual take-home will be lower once you account for income tax. But net profit margin is still the most useful number for understanding business health. Tax is calculated separately based on your jurisdiction's rules.

What Healthy Profit Margins Look Like for Sleep Consultants

Sleep consulting is a service business with almost no cost of goods. You're not buying inventory or materials to deliver your service. This means your profit margins should be significantly higher than a product-based business.

| Profit margin | What it signals | What to look at |

|---|---|---|

| 75%+ | Excellent. Lean, profitable, sustainable. | Consider whether your pricing reflects your experience and demand |

| 60–75% | Healthy. Normal for a growing business investing in tools. | Review whether all subscriptions are earning their cost |

| 40–60% | Manageable, but expenses are high relative to revenue. | Audit every expense line. Is everything necessary right now? |

| Below 40% | Warning sign. You may be underpriced or overspending. | Review pricing, cut non-essential tools, and talk to an accountant |

For context: most service businesses consider a 10–20% net profit margin acceptable. Sleep consulting, as a solo practice with low overhead, should be performing significantly above that. If you're not, the usual culprits are pricing that's too low, expenses that have crept up unnoticed, or both. See How to Price Your Sleep Consulting Services if your margins are telling you something about your rates.

The Profit and Loss Statement

A Profit and Loss statement (P&L, also called an income statement) is simply a structured view of the three numbers above, covering a specific time period. Think of it as a health check-up for your business. It shows you at a glance whether you're making money, and if not, exactly where the gap is.

A basic P&L for a sleep consulting business looks like this:

Run this for your business every month, even if it only takes ten minutes. The habit of seeing the numbers regularly is what builds financial clarity, and financial clarity is what lets you make good decisions about pricing, investment, and growth.

Bookkeeping Basics: Tracking Income and Expenses

Bookkeeping is simply the practice of recording every financial transaction your business makes. It doesn't need to be complicated. At the start, all it means is that every time money comes in or goes out, you write it down somewhere.

Option 1: A spreadsheet

A Google Sheet or Excel file with columns for date, description, income, expense, and category is enough to start. Create a new tab for each month. At the end of the month, total the income column, total the expense column, subtract one from the other, and you have your net profit. Simple, free, and completely sufficient for a new sleep consulting business.

Option 2: Accounting software

Once you're earning consistently, accounting software automates much of the tracking, connecting to your bank account, categorising transactions, and generating P&L reports automatically. It also simplifies working with an accountant, since all your data is in one organised place. Research what's available and popular in your country, as options and pricing vary.

The one non-negotiable: separate bank accounts

All business income goes into a business bank account. All business expenses come out of that same account. Personal transactions stay in your personal account. Mixing the two creates chaos at tax time, makes bookkeeping nearly impossible, and (if you're operating as an LLC) can legally compromise the liability protection the structure provides. This is the single most important financial habit to build from day one.

Also open a separate savings account specifically for tax. After every client payment, transfer a percentage into it immediately (more on the percentage in the next section). You'll thank yourself every time tax season arrives.

Tax: How Much to Set Aside and When to Pay

The most common financial mistake new sleep consultants make is spending all their income as it arrives, and then getting hit with a tax bill they can't pay. The solution is simple: set aside a percentage of every payment the moment it lands, before you spend anything else.

A general starting point is to set aside 25% of your income for taxes. If you're in a lower income bracket or your country has lower tax rates, the actual amount may be less. If you're in a higher bracket, it may be more. Check with a local accountant or tax authority to get a figure specific to your situation, but 25% is a reasonable default to start with while you figure out your actual liability.

USA: Self-employed individuals typically pay quarterly estimated taxes (April, June, September, January). You'll also pay self-employment tax (Social Security and Medicare) on top of income tax. UK: Self-assessment tax return filed annually by 31 January. Payments on account may be required twice a year once income exceeds a threshold. Australia: BAS (Business Activity Statement) filed quarterly if registered for GST; personal income tax filed annually. Canada: Quarterly instalment payments required if your tax owing exceeds CAD $3,000 in the current or prior year. Netherlands: Quarterly VAT return if VAT-registered; annual income tax return. New Zealand: Provisional tax paid in three instalments across the year. South Africa: Provisional tax paid twice a year (August and February). All countries: rules change. Verify current requirements with your local tax authority or an accountant.

Depending on your country and income level, you may also need to register for VAT, GST, or a local equivalent once your revenue crosses a certain threshold. In many countries this threshold is well above what a new sleep consultant earns in their first year, but it's worth knowing the number in your jurisdiction so you're not caught off guard when you get there.

Ongoing Compliance: Licences, Permits, and Annual Filings

Compliance is not exciting, but missing a deadline can result in fines, penalties, or your business registration lapsing. Build a simple compliance calendar at the start of each year with all your key dates.

Depending on your location and structure, ongoing compliance may include:

- Annual business registration renewal. Many jurisdictions require you to renew your business registration or file an annual report. For LLCs this is usually $50–$200 per year. Missing it can result in your registration being cancelled.

- Local business licence. Some cities or municipalities require a local business licence to operate, even for a home-based service business. Check your local government website to confirm whether this applies to you.

- Professional certification renewal. Your sleep consultant certification may require continuing education or periodic renewal. Keep track of when yours expires.

- Insurance renewal. Professional liability and general liability insurance need to be renewed annually. Review coverage when you renew. Your needs may have changed.

- Tax deadlines. Income tax, quarterly estimates, VAT/GST returns: all have deadlines that vary by country. Put them all in a calendar with a reminder two weeks before each one.

Frequently Asked Questions

Do I need an accountant as a new sleep consultant?

Not immediately for day-to-day bookkeeping. A spreadsheet handles things perfectly well when you're starting out. But for your first tax return, and ideally once a year thereafter, yes. An accountant who works with small service businesses or sole traders will save you more in tax than they cost, catch things you'd miss, and give you peace of mind that everything is filed correctly. Think of it as an investment rather than an expense.

What if my business is making a loss in the early months?

A loss in the first few months is common and expected. You're investing in setup costs before revenue has fully built. The important thing is to track it accurately, understand what's causing it (typically startup expenses rather than ongoing costs), and have a realistic timeline for when revenue will exceed expenses. In most countries, business losses can be offset against other income or carried forward to future tax years, which is another good reason to keep accurate records from day one.

Should I charge sales tax or VAT on my services?

This depends entirely on your country, your annual revenue, and what type of service you're providing. In many countries, VAT or GST registration is only required once your revenue crosses a threshold, and even then some professional services may be exempt. In the US, most services (as opposed to products) are not subject to sales tax, though this varies by state. This is a question to answer with a local accountant or by checking your country's tax authority website directly.

How do I pay myself from my business?

As a sole trader, your business profit is your income. You transfer money from your business account to your personal account as needed. As an LLC or Ltd, you typically pay yourself either a salary (which creates payroll obligations) or a draw/dividend (which has different tax implications depending on your jurisdiction). The right approach depends on your structure and country. An accountant familiar with your setup is the best guide here.

What records do I need to keep, and for how long?

Most tax authorities require you to keep financial records for a minimum of 5 to 7 years, though the exact period varies. This includes invoices you've issued to clients, receipts for every business expense, bank statements, and copies of your tax returns. Store everything digitally in a dedicated folder (Google Drive or similar), organised by year. A labelled receipt photographed on your phone and saved immediately is infinitely better than a crumpled receipt found at tax time six months later.

Key Takeaways

- Know your three numbers: revenue, expenses, and net profit margin. If you don't know them right now, this week's task is to calculate them.

- A healthy profit margin for a solo sleep consulting business is 60–75%+. Service businesses have structural advantages. Use them.

- Separate your finances from day one. Business account for business. Personal account for personal. No exceptions.

- Set aside 20–30% of every payment for tax before you spend anything else. Into a dedicated savings account, immediately.

- Start with the simplest business structure that fits your situation. Most new sleep consultants start as sole traders and upgrade to an LLC or Ltd once earnings are consistent.

- Build a compliance calendar. One document, all your renewal dates and tax deadlines, reminders set two weeks ahead of each one.

- Get an accountant for your annual tax return at minimum. The cost is almost always worth it, and in many countries the fee is itself a deductible business expense.

You don't need to love numbers to run a financially healthy business. You just need to know three of them, check them once a month, and build the habits that keep you protected and compliant. Start with this month's P&L. It takes ten minutes and tells you everything you need to know.

Next Article: How to Price Your Sleep Consulting Services

Disclaimer: The information shared in these articles is for educational and informational purposes only. It does not constitute legal, financial, or professional advice. Always consult with a qualified professional regarding your specific situation.

Rianna Hijlkema

Certified Pediatric Sleep Consultant, Certified Postpartum Doula, Former Teacher & School Director, Founder of Sleep Consultant Design & Sleep Consultant Business and the author of The Sleep Consultant Playbook (available on Amazon).

The Sleep Consultant Newsletter

Weekly tips, strategies and marketing ideas for sleep consultants written by a fellow sleep consultant. 1500+ active subscribers!

I’ll only send helpful emails, and you can unsubscribe anytime with one click.

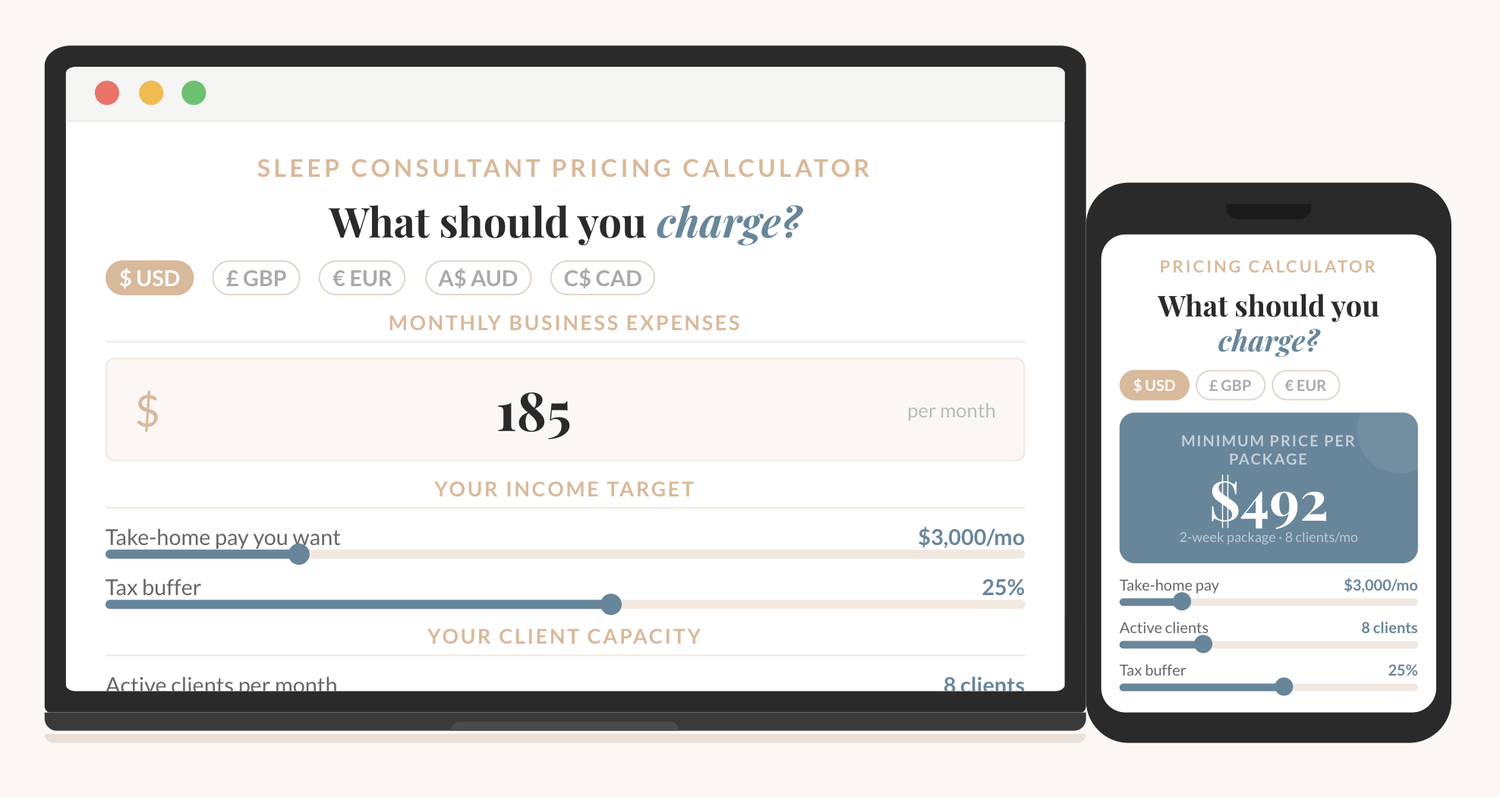

How to price your sleep consulting services?

The Sleep Consultant Pricing Calculator shows you exactly what to charge, based on your real expenses, your income goal, and how many clients you want to take on.

I'm thrilled to offer you an exclusive preview of what’s inside!

You can read the first 22 pages of The Sleep Consultant Playbook and get a taste of the value, insights, and actionable strategies that are waiting for you.

Other articles you might be interested in:

© 2021-2026 Sleep Consultant Business. All Rights Reserved.